Losing Free COBRA Premiums or Job Health Insurance? You Can Still Enroll in Health Coverage for the Last Few Months of 2021

Residents with a Qualifying Event Have Options to Get Covered

DENVER – Thousands of Coloradans will lose free COBRA premiums at the end of the month and may need other affordable coverage options. Through the American Rescue Plan Act, which passed earlier this year, many people were able to receive free COBRA premiums through September 30. Connect for Health Colorado, the state’s health insurance marketplace, is reminding residents that they can still sign up for a health insurance plan for the remainder of the year if they experience a Qualifying Life Event, such as losing free COBRA premiums this month or losing job health insurance.

Methodology reminders, including some important updates:

I go by FULLY vaccinated residents only (defined as 2 doses of the Pfizer or Moderna vaccine or one dose of the Johnson & Johnson vaccine).

I base my percentages on the total population, as opposed to adults only or those over 11 years old.

For most states + DC I use the daily data from the Centers for Disease Control, but there are some where the CDC is either missing county-level data entirely or where the CDC data is less than 90% complete at the county level. Therefore:

For California, I'm using the CDC data for most counties and the state health dept. dashboard data for the 8 small counties which the CDC isn't allowed to post data for.

The 5 major U.S. territories don't vote for President in the general election, preventing me from displaying them in the main graph, but I have them listed down the right side.

Assuming the first case was ~December 15th or so, it was roughly 325 days from then until the Presidential Election on November 3rd, 2020, or a little under 11 months.

It's been 327 days from Election Day through September 26, 2021.

In other words, almost exactly as much time has passed in the post-election phase of the COVID pandemic as in the pre-election phase.

Nebraska doesn't even bother listing indy/small group plan rate filings on their own insurance department website...the link goes directly to the federal Rate Review database. The problem with this is that very few filings here are unredacted, which means it's difficult to acquire the policy enrollees for many carriers needed to run a weighted average.

Fortunately, Nebraska has only 3 carriers for 2022...one of which is brand new to the state (Oscar Health), and of the other two, Medica's filing summary does include an exact number of enrollees. That leaves just Bright Health, and since I know (roughly) how many enrollees are in Nebraska's overall indy market, voila: 8.6% average rate increases.

On the other hand, I don't have the enrollment for any of the 4 Small Group market carriers. It also looks like UnitedHealthcare is pulling out of the NE sm. group market, but it might just be that the federal database doesn't have them listed yet (I doubt this since it's so close to the Open Enrollment Period). The unweighted average rate change is a 2.1% reduction:

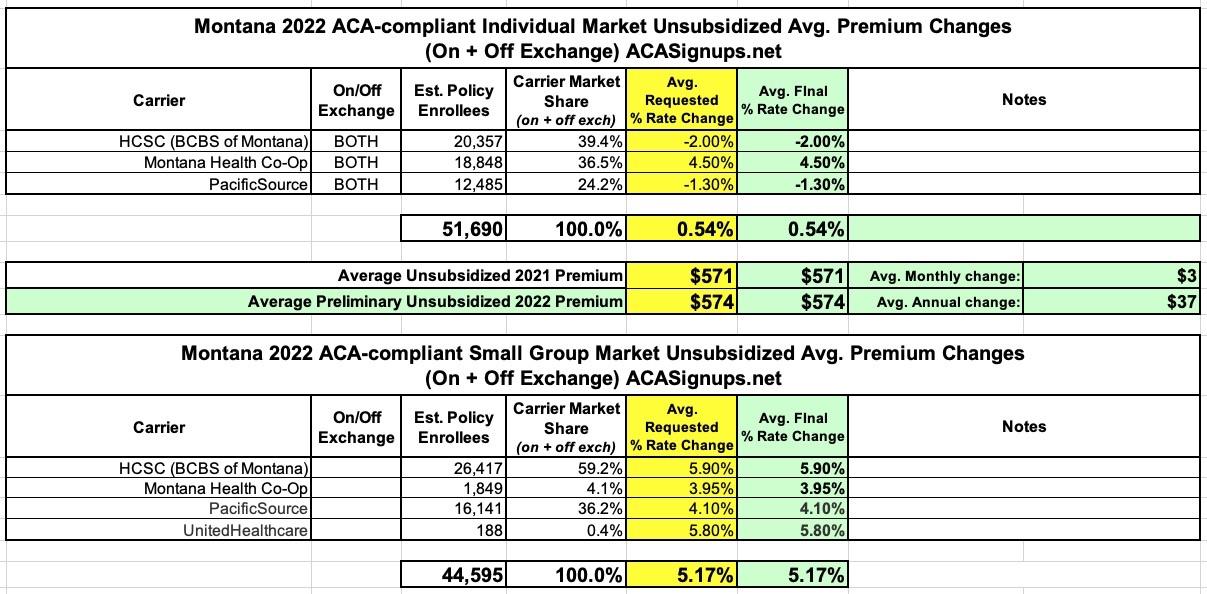

Seriously, if every state displayed their annual rate filing data in as simple and clear-cut a fashion as Montana does, I'd be a much happier man. Admittedly, several others do, but the trickiest issue is usually getting the estimated enrollment numbers.

In any event, not much to say about Montana's ACA markets in 2022: No new carriers are jumping in, no current ones are dropping out, and the rate changes are pretty straightforward: +0.5% on the individual market, +5.2% on the small group market.

UPDATE 10/22/21: Well, it looks like the Montana Insurance Dept. has signed off on all 7 rate filing requests without making any changes, so I guess these are the approved rate changes as well:

Georgia's health department doesn't publish their annual rate filings publicly, but they don't hide them either; I was able to acquire pretty much everything via a simple FOIA request which was responded to within a few hours of my asking.

As of 2021, there are six insurers that offer exchange plans in Georgia. Five additional insurers plan to join them for 2022: Friday Health Plans, Bright Health, Aetna, UnitedHealthcare, and Cigna (Aetna, UHC, and Cigna all participated in Georgia’s exchange previously, but left at the end of 2016).

It's worth noting that each market has a new entrant for 2022: Aetna is joining the individual market while Cigna is jumping into the off-exchange Small Group market.

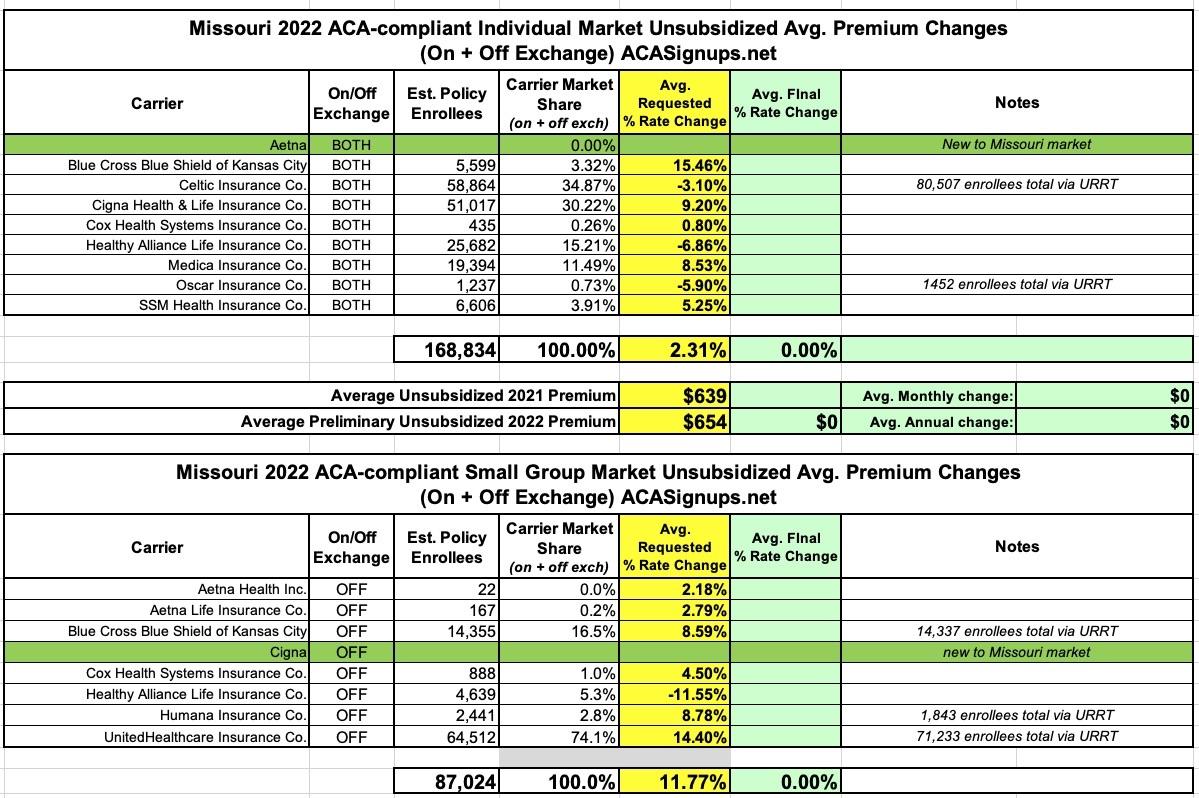

The differences in enrollment noted for some carriers is likely due to some product lines being discontinued--for instance, if Celtic drops premiums by 3.1% on most of their policies but discontinues some others entirely, those enrolled in the discontinued lines won't have any official rate change to their existing policies.

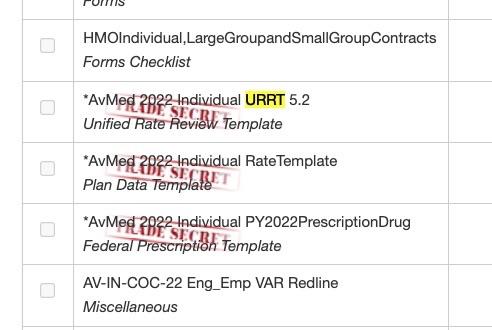

Florida state law apparently gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret."

In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

Cigna is joining the Mississippi exchange for 2022, bringing the total number of participating insurers to three. According to ratereview.gov, the following average rate changes have been proposed by Mississippi’s current exchange insurers: